The Systems Running Your Financial Life While You Are Not Looking

Nobody sits a young person down and explains the machinery.

You get the job. You sign the paperwork. You show up, do the work, and wait for payday with a number in your head based on what you were told you would earn. And then the paycheck arrives and the number is smaller. Sometimes significantly smaller. And the natural human response is confusion followed by a quiet acceptance that this is simply how it works, without ever fully understanding why.

That acceptance is understandable. But it is also expensive.

Because the financial systems operating in the background of most people’s lives are not random. They are not accidental. They are structured, consistent, and in many cases, designed to collect from people who are not paying close enough attention to notice. Understanding them does not require a finance degree. It requires the willingness to look at something most people prefer to leave blurry.

This is what the machinery actually looks like.

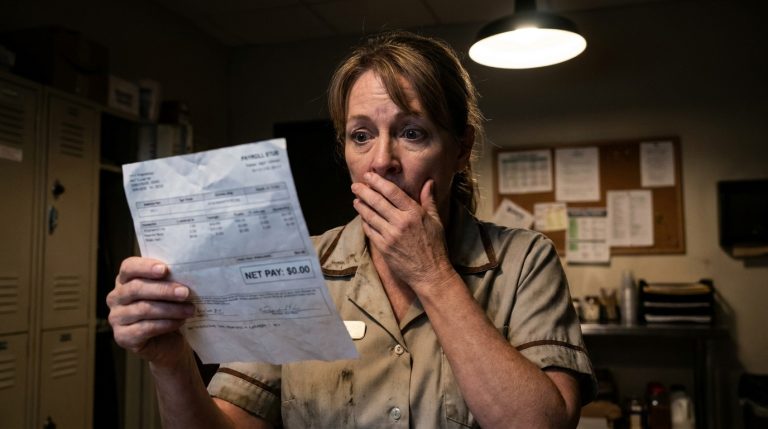

The Paycheck That Was Never the Full Number

The first hidden system most working people encounter is payroll deduction. And it introduces itself on the very first payday of your working life.

You were offered a salary or hourly rate during the hiring process. That number is your gross income. What lands in your account is your net income. The distance between those two numbers is occupied by a collection of deductions that were always going to be there, whether or not anyone explained them to you beforehand.

Federal income tax comes out first. Then state income tax, depending on where you live. Then Social Security contributions at six point two percent of your wages. Then Medicare at one point four five percent. If your employer offers health insurance and you opted in, that premium comes out too. If there is a retirement plan contribution, that reduces the number further.

By the time the paycheck reaches you, it has already funded obligations you may not have consciously agreed to in any meaningful sense. You agreed in the general sense of living in a society with a tax structure. But the specific mechanics were likely never walked through with you in plain language before your first check arrived short.

For most workers this gap between expected and received pay is the first real introduction to the idea that financial systems operate independently of your awareness of them.

Interest: The Cost That Never Stops

Consider a man named Daniel. He is twenty six years old and recently took out a car loan for eighteen thousand dollars at an interest rate of seven percent over five years.

The monthly payment is manageable. He checked that before signing. What Daniel did not sit down and calculate is the total cost of the loan by the time the final payment clears.

Over five years at seven percent interest Daniel will pay approximately three thousand and sixty dollars in interest alone. He is not buying an eighteen thousand dollar car. He is buying a twenty one thousand dollar car and receiving it eighteen thousand dollars at a time.

Interest is the cost of using money that is not yours yet. And it operates on a schedule that continues running whether you think about it or not. Every month that passes with a balance on a loan, a mortgage, or a credit card, the interest calculation runs. It does not wait for a convenient moment. It does not pause when money is tight. It simply accrues.

The inverse of this is what makes investing work. The same compounding mechanism that quietly costs borrowers money over time quietly builds wealth for those who put money into assets. The system is neutral. It simply runs in whichever direction the money is flowing.

Credit Card Debt and the Minimum Payment Trap

The credit card is perhaps the most sophisticated and widely misunderstood financial instrument most people carry in their wallet.

It offers convenience, rewards, and the ability to spend money that has not been earned yet. For someone who pays the full balance every month, it is a genuinely useful tool. For someone who carries a balance, it is one of the most expensive financial arrangements available in ordinary consumer life.

The average credit card interest rate in the United States sits above twenty percent annually. This means that a balance of five thousand dollars, left untouched and serviced only by minimum payments, can take over fifteen years to eliminate and cost more than five thousand dollars in interest over that period.

The minimum payment exists by design. It keeps the account in good standing. It prevents the penalty fees that come with missed payments. And it extends the life of the balance for as long as mathematically possible, which is precisely the period during which interest continues to compound.

Most people carrying credit card debt are not irresponsible. They are caught in a system they did not fully understand when they signed up for the card and have not had explained clearly since. The solution is not shame. It is arithmetic. Knowing exactly what a balance costs over time changes the urgency with which it gets paid down.

Fees: The Smallest Numbers With the Longest Reach

There is a particular category of financial drain that operates almost entirely below the level of conscious attention. Fees.

Late payment fees. Overdraft fees. Subscription fees for services no longer being used. Annual fees on financial products that no longer serve their original purpose. ATM fees for using a machine outside your bank’s network. Foreign transaction fees on cards used while traveling.

Individually, these numbers feel small. Fifteen dollars here. Thirty five dollars there. Monthly charges of nine ninety nine that have been quietly renewing for two years on a streaming service last accessed in a different season of life.

Collectively, across a year, these amounts can represent hundreds of dollars redirected away from savings or debt repayment without a single deliberate decision being made. They are the financial equivalent of a slow leak. Not dramatic enough to trigger alarm. Consistent enough to matter significantly over time.

The practical response to fees is a simple audit. Once a year, going through every recurring charge on every bank and credit card statement, is one of the highest return per hour financial activities available to anyone. The ones that are no longer serving a purpose get cancelled. The ones generating fee income for institutions without delivering proportional value get renegotiated or replaced.

The Late Fee Spiral

Late fees deserve their own consideration because of the way they compound psychologically as well as financially.

Missing a payment because of a tight month is common. The late fee that follows makes the next month tighter. The next month being tighter increases the likelihood of another missed payment. Another missed payment triggers another fee and potentially a penalty interest rate that replaces the original rate with something significantly higher.

This is a spiral that starts with a single moment of financial pressure and accelerates through a system designed to collect more when the borrower is already strained. It is legal. It is disclosed in the fine print. And it catches people every day who did not fully absorb what the fine print meant when they signed.

Breaking the spiral requires understanding its mechanics well enough to prioritize strategically. Minimum payments on accounts with penalty rate triggers often take precedence over larger payments on lower interest debt, simply because the cost of triggering the penalty rate outweighs the benefit of the extra principal payment elsewhere.

The System Is Not Personal

What is important to understand about all of these mechanisms, payroll deductions, interest, fees, minimum payments, late charges, is that they are not targeted at individuals. They are simply systems. Structures that run consistently and collect predictably from everyone they touch equally.

The person who understands them navigates differently than the person who does not. Not because they earn more or have more discipline. Because they can see the machinery clearly enough to make decisions that account for it.

A young woman who understands that carrying a credit card balance at twenty two percent interest is effectively paying a fee for the privilege of spending future money makes different decisions than one who does not. A worker who understands that payroll deductions will reduce their take-home pay by a significant percentage does not build a monthly budget around the gross number. A borrower who runs the total interest calculation on a loan before signing does not just check whether the monthly payment fits.

Financial literacy is not about becoming immune to these systems. Nobody is. It is about seeing them clearly enough to stop being surprised by them and start building a life that accounts for their presence.

The Closing Observation

The money you earn passes through several systems before it reaches you. And after it arrives, other systems are already positioned to collect portions of it, quietly and consistently, for as long as you carry balances, subscribe to services, miss deadlines, or borrow against a future that has not arrived yet.

None of this is hidden in the conspiratorial sense. It is all disclosed somewhere. In the paperwork. In the terms. In the fine print that most people sign without reading because the document is long and the moment is inconvenient.

But disclosed and understood are two different things entirely.

The most financially empowering shift a person can make is not earning more. It is deciding to understand clearly, once and for all, exactly how the machinery works.

Because a system you can see clearly is a system you can finally start to navigate.