The Boring Path Is the Only Path

Nobody posts about the Tuesday night they stayed home and moved five hundred dollars into an index fund instead of going out.

Nobody makes a highlight reel of the third consecutive year they drove the same car, lived in the same modest apartment, and said no to the vacation everyone else was taking. There is no viral moment in watching a number on a screen grow by small, almost invisible percentages over months and years. There is no applause for the decision that costs you nothing dramatic and gains you nothing immediately visible.

And yet that quiet, unglamorous, deeply ordinary sequence of choices is almost always the actual story behind generational wealth.

The version of wealth-building that gets attention is the exception. The startup that sold for forty million. The crypto trade that returned ten thousand percent. The influencer who turned a following into a fortune. These stories are real. They happen. But they are statistical outliers being presented to millions of people as if they are the standard path, and the gap between that illusion and reality is quietly costing people their financial futures.

The actual path is slower. It is less interesting. And for the person on it, it requires something far more demanding than a single bold move. It requires the willingness to be ordinary, consistently, for a very long time.

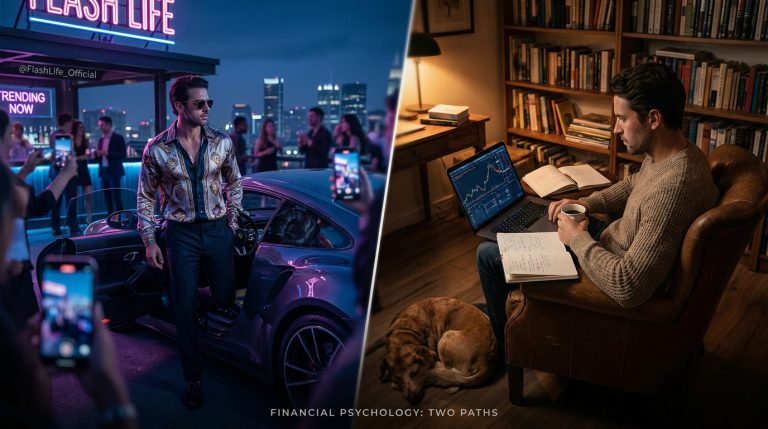

The Illusion Being Sold Every Day

Open any financial content platform on any given day and you will find a version of the same story. Someone young. Someone who was recently broke or struggling. Someone who discovered a strategy, a system, an asset class, and then everything changed quickly.

The story is structured to feel both inspirational and accessible. If they could do it, so can you. And the implication, always, is that the transformation was relatively swift. The before and after compressed into a digestible narrative that leaves out the decade of compounding, the years of living below their means, or the inheritance nobody mentions.

This is not always dishonest. But it is almost always incomplete.

And the incomplete story does something insidious to the people consuming it. It recalibrates their expectations. It makes the slow, consistent approach feel like settling. It makes the person quietly contributing to their retirement account every month feel like they are missing the real game happening somewhere else.

They are not missing anything. They are playing the only game that reliably works. They just cannot see the scoreboard yet.

What Discipline Actually Looks Like From the Inside

There is a woman named Grace. She is thirty six years old and works as a mid-level project manager at a logistics company. Her income is comfortable but not extraordinary. She does not work in finance. She has never started a company. She has no side hustle generating passive income at scale.

What Grace has done, since the age of twenty four, is contribute consistently to her employer’s retirement plan, invest a fixed percentage of every paycheck into a low-cost index fund, and live on a budget that has not expanded proportionally with her salary.

When she got promoted at twenty nine and her income increased by twelve thousand dollars a year, she did not upgrade her apartment. She increased her investment contributions and kept her lifestyle largely the same. When her colleagues began leasing new cars, she repaired her existing one. When the group chat started planning an expensive international trip, she went for one week instead of two and put the difference into her brokerage account.

From the outside, Grace does not look like someone with a financial story worth telling. She is not flashy. She does not talk about money much. She drives an unremarkable car and brings lunch to the office more days than not.

But Grace, at thirty six, has an investment portfolio most people twice her age have not built. Not because she earned more than them. Because she never stopped the quiet, boring, consistent work of building while everyone else was funding the appearance of having already arrived.

Her story will never go viral. But it is the most important financial story most people will never hear.

The Psychology of Lifestyle Inflation

One of the most powerful and least discussed forces working against wealth accumulation is the near-universal human tendency to expand spending as income grows.

It feels natural. It feels earned. After years of working hard and earning more, the idea of continuing to live the same way feels like deprivation. And in a culture that constantly signals that spending is the appropriate reward for success, resisting that pull requires a kind of psychological clarity that most financial education never addresses.

Lifestyle inflation is not simply about buying more expensive things. It is about the gradual, almost unconscious raising of the baseline. The restaurant that used to feel like a treat becomes the regular Tuesday option. The vacation that was once a special occasion becomes the annual minimum. The apartment upgrade that felt like a reward becomes the new floor from which the next upgrade is measured.

Each individual step feels reasonable. Collectively, they consume the exact gap between income and wealth.

The people who build real wealth over time are not necessarily earning dramatically more than their peers. They are simply protecting the gap. They are treating the distance between what they earn and what they spend as sacred territory, not to be invaded by comfort, status, or social pressure.

They understand something that takes most people decades to learn. That financial freedom is not built by earning more. It is built by consistently spending less than you earn and directing the difference toward assets that grow without your daily attention.

The Compound Effect and Why It Feels Like Nothing

Albert Einstein is often credited with calling compound interest the eighth wonder of the world. Whether he said it or not, the mathematics behind the idea are genuinely extraordinary and genuinely invisible until they are not.

The reason most people abandon long-term wealth-building strategies is not laziness. It is the complete absence of feedback in the early years. You contribute for twelve months and the account has grown but not in any way that changes your life visibly. You contribute for three years and the number is larger but still feels abstract. The sacrifice is immediate and real. The reward is theoretical and distant.

This is the psychological barrier that separates the people who build wealth from the people who intend to.

Because at year ten, something changes. At year fifteen, the growth starts to feel real. At year twenty, the number on the screen is doing things that your monthly contributions alone could never explain. The interest is earning interest. The dividends are compounding. The asset you built quietly and consistently in the background has taken on a momentum of its own.

But you have to stay in the game long enough to reach that moment. And most people do not, because the early years offer nothing exciting enough to hold their attention against a world full of things competing for both their focus and their money.

Why the Wealthy Live Below What They Could

One of the most consistent findings across studies of high net worth individuals is that genuine wealth and visible wealth are far less correlated than most people assume.

The research that became the foundation of the book on millionaire next door behavior found that a significant proportion of genuinely wealthy people in America lived in modest homes, drove ordinary vehicles, and spent carefully in ways that made them functionally invisible against their actual net worth.

This is not because wealthy people are joyless or ascetic. It is because their relationship with money is fundamentally different from the person using spending as a signal of status. The wealthy person has already internalized their success. They do not need the car to tell the story because they can read the account balance directly.

They have also learned, through experience or observation, that the lifestyle built on appearance requires constant and expensive maintenance. That every upgrade creates a new baseline. That the image of wealth and the experience of actual financial freedom are not just different things, they are frequently in direct opposition to each other.

Living below your means, for someone who has built real wealth, is not sacrifice. It is simply the habit that got them there, maintained long enough to become identity.

The Closing Observation

The most important financial decision most people will ever make is not a single bold move. It is the quiet, repeated, unspectacular choice to keep going when nothing visible is happening.

To keep contributing when the market is flat. To keep living simply when everyone around you is upgrading. To keep saying no to the thing that would feel good today in service of the thing that will matter in twenty years.

Wealth is not built in the moments that get attention. It is built in the ones nobody ever sees.

And the people who understand that early enough are the ones who eventually have nothing left to prove.