Tax Free and Tax Deduction Are Not the Same Thing

The rumor spread the way most financial misinformation does. Quietly, quickly, and through people who were genuinely trying to be helpful.

It started showing up in break rooms and group chats. Someone had heard it from a coworker who heard it from a friend who had seen something about it online. The message was simple and exciting. Tips are tax free now. You do not have to pay taxes on your tips anymore.

For millions of tipped workers living on unpredictable income, the idea was more than welcome. It felt like relief. It felt like finally, after years of watching a significant portion of hard-earned gratuity disappear into withholding and tax bills, something had shifted in their favor.

The problem was that the message was wrong. Not entirely fabricated, but wrong in the way that half-truths are often more dangerous than complete fiction. Because a half-truth gives a person just enough confidence to stop asking questions.

And in personal finance, stopping too early is where the damage begins.

What Actually Happened

What was being discussed, and what many people genuinely misunderstood, was a proposed tax deduction on tip income. Not an exemption. Not a removal of tax liability. A deduction.

These two things sound similar. They are not. And the gap between them, when misunderstood, can result in financial decisions built on a foundation that does not exist.

To understand why the distinction matters so deeply, it helps to start with something more fundamental. What taxable income actually is and how the government decides how much of your money it is owed.

How Taxable Income Works

When you earn money, whether through an hourly wage, a salary, freelance work, or tips left on a table, the government counts that as income. All of it, in most cases, begins as gross income. The total amount you earned before anything is taken out.

But the government does not typically tax your gross income directly. It taxes your taxable income, which is your gross income after certain allowances, adjustments, and deductions have been subtracted. The goal of these subtractions is to arrive at a number that more accurately reflects your financial reality before calculating what you owe.

This is where deductions enter the picture. And where the confusion around tips began.

What a Deduction Actually Is

A deduction is a reduction in the amount of income that is subject to tax. It does not eliminate your tax liability. It lowers the number from which your tax liability is calculated.

Here is a straightforward example. Imagine you are a server who claims forty thousand dollars in tips over the course of a year. Under a proposed tip deduction with a maximum of twenty five thousand dollars, you would subtract twenty five thousand from forty thousand. Your taxable tip income would then be fifteen thousand dollars rather than forty thousand.

You are still being taxed. You still owe money on that fifteen thousand. But you owe significantly less than you would have if the full forty thousand had been taxed.

That is a deduction. It is a meaningful financial benefit. But it is not the same thing as paying nothing. And for anyone who planned their finances around the assumption that their tip income would become completely untaxable, the difference is not a technicality. It is a real and potentially significant amount of money they were not expecting to owe.

Tax free means zero tax owed on that income. A deduction means less tax owed. These are different outcomes. And confusing them can leave a person financially exposed at exactly the moment they thought they were protected.

Why the Misunderstanding Happens

The financial literacy gap in most countries is wide. And it is not the result of people being careless or unintelligent. It is the result of a system that is genuinely complex being left almost entirely to individuals to decode on their own.

Most people learn about taxes the first time taxes affect them directly. Not in school. Not from a trusted adult sitting down to walk them through it. But on the job, in real time, often after a decision has already been made based on incomplete information.

Consider a young woman named Aaliyah. She is nineteen years old and just started her first job as a server. She is sharp, motivated, and eager to manage her money well. She hears from two colleagues during her first week that tips are tax free. She trusts them because they have worked there longer and because the information is delivered with confidence.

She adjusts her behavior accordingly. She stops setting money aside from her nightly tips. She spends more freely through the year because she believes her tax bill will be smaller than it actually will be. And then tax season arrives and she is looking at a number she did not budget for because the premise she built her year on was never accurate.

Aaliyah did not fail. The system failed her. The information that should have been available, clearly and early, was not. And the misinformation that filled the gap was offered with good intentions and no accountability.

This is how financial literacy gaps cost ordinary people real money.

Payroll Withholding and the Confusion It Adds

The situation becomes even more layered when you factor in how taxes are collected throughout the year rather than all at once at the end.

Payroll withholding is the system by which your employer deducts estimated taxes from each paycheck before you ever receive it. For salaried workers, this process is relatively predictable. But for tipped workers, it creates a dynamic that surprises nearly everyone who encounters it for the first time.

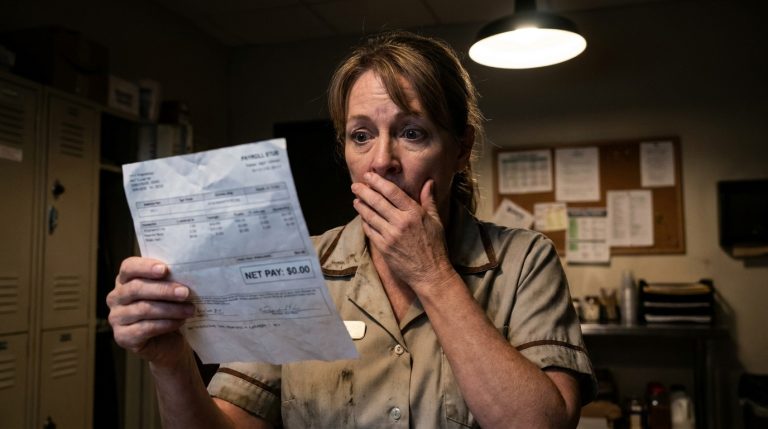

When a tipped worker claims their tips at the end of a shift, those tips are recorded as income for that pay period. The taxes estimated to be owed on that income are then withheld from the worker’s base hourly paycheck, because that is the only channel available for collection. The tip money has already been taken home in cash.

At a base wage of two dollars and thirteen cents per hour, there is very little cushion in that hourly paycheck to absorb a tax bill. In weeks with strong tip income, the withholding can consume the entire base wage and produce a paycheck that reads zero.

This system is not designed to punish tipped workers. It is simply the mechanism of collection applied to a pay structure the mechanism was not originally designed for. But the result, for workers who do not understand it, can feel like something has gone wrong when nothing unusual has happened at all.

If someone in that position also believed their tips were completely tax free, they would be experiencing two layers of confusion simultaneously. The zero paycheck would feel inexplicable and the tax bill at year end would feel like a betrayal.

Both outcomes trace back to the same root. Not understanding how the system works before it starts working on them.

Why Understanding This Early Changes Everything

There is a version of financial life that is reactive. You earn, you spend, and you deal with the consequences of taxes and bills when they arrive. Most people live here by default, not by choice.

And then there is a version that is proactive. You understand the system well enough to anticipate it. You know that tip income is taxable. You know that a deduction lowers your taxable income but does not eliminate it. You set aside a percentage of your tips through the year so that tax season does not become a financial emergency. You understand your withholding elections and revisit them when your income changes significantly.

The difference between these two versions of financial life is not income. It is knowledge applied early enough to matter.

A person who understands the difference between tax free and a deduction before they need to is not just better prepared for tax season. They make better decisions all year. They save more intentionally. They are not caught off guard by systems that were always going to work exactly the way they worked.

Financial literacy is not about becoming an expert. It is about knowing enough to ask the right questions before the wrong assumptions cost you.

The Closing Insight

Words matter differently in finance than they do in conversation.

In everyday language, tax free and tax reduced might feel close enough that the distinction barely registers. In the context of your actual money, they represent two completely different outcomes. One means you owe nothing. The other means you owe less. And building your financial plans around the wrong one is a mistake that often does not reveal itself until long after the decision was made.

The most important financial skill most people are never taught is also one of the simplest.

Understand exactly what a word means before you let it change what you do with your money.